Private equity firms are under constant pressure to deliver returns.

Deals are competitive.

Valuations are high.

Holding periods are tighter.

And the expectation is clear:

Create value. Fast.

To do that, most firms turn to private equity consulting, and in many cases, private equity operations consulting.

Strategy advisors. Operating partners. Transformation consultants.

But there’s a growing realization across the industry:

Consulting alone doesn’t drive EBITDA.

Execution does.

The Problem: Value Creation Plans Don’t Equal Results

Every private equity firm has a value creation plan.

It typically includes:

- Cost reduction initiatives

- Operational improvements

- Supply chain optimization

- Digital and AI transformation

- Growth and commercial strategies

On paper, these plans are sound.

In practice, they often fall short.

Research shows that 70–90% of strategic initiatives fail to achieve their intended value

Private equity is not immune to this.

The issue isn’t identifying opportunities.

It’s implementing them inside portfolio companies.

What Private Equity Consulting Actually Delivers

Private equity consulting firms—and teams focused on value creation consulting for private equity—play an important role in the deal lifecycle.

They support:

- Commercial due diligence

- Operational assessments

- Value creation planning (often via value creation consulting for private equity)

- Benchmarking and analysis

This work helps firms:

- Identify upside opportunities

- Quantify value creation potential

- Prioritize initiatives

But this is where most engagements stop.

What gets delivered:

- A roadmap

- A business case

- A list of initiatives

What’s missing:

- Execution at the portfolio company level

- Integration into day-to-day operations

- Sustained operational change

The result:

Clear plans.

Limited EBITDA impact.

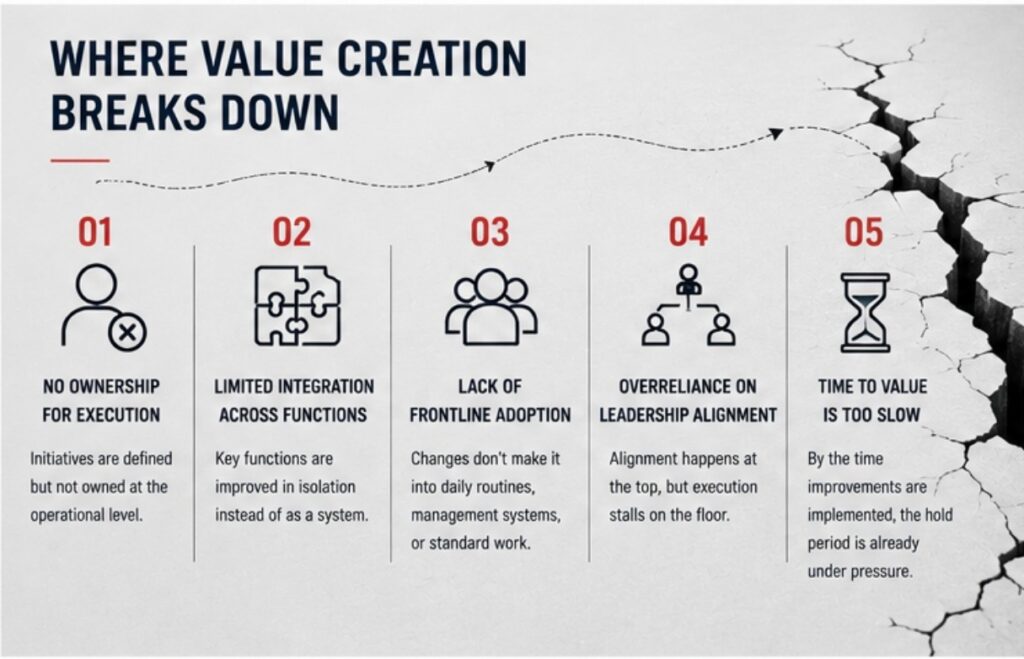

Where Value Creation Breaks Down

The gap between consulting and results shows up in the same places across portfolio companies:

1. No Ownership for Execution

Initiatives are defined but not owned at the operational level.

2. Limited Integration Across Functions

Operations, supply chain, maintenance, and quality are improved in isolation instead of as a system.

3. Lack of Frontline Adoption

Changes don’t make it into daily routines, management systems, or standard work.

4. Overreliance on Leadership Alignment

Alignment happens at the top, but execution stalls on the floor.

5. Time to Value Is Too Slow

By the time improvements are implemented, the hold period is already under pressure.

Value Creation: Where EBITDA Is Actually Driven

EBITDA doesn’t improve because of a plan.

It improves when operational performance changes.

Across portfolio companies, the biggest drivers of EBITDA are:

Throughput Improvement

More output from existing assets.

- Bottleneck removal

- Flow optimization

- Scheduling improvements

Cost Reduction That Sticks

Not one-time cuts—structural improvements.

- Labor productivity

- Waste elimination

- Process efficiency

Asset Reliability

Unplanned downtime directly erodes EBITDA.

- Predictive maintenance

- Better maintenance execution

- Integrated operations and maintenance

Quality and Yield

Scrap and rework are hidden margin killers.

- Early defect detection

- Standardized quality processes

- Embedded quality systems

Planning and Execution

Most inefficiencies start upstream.

- Demand forecasting

- Production planning

- Inventory optimization

These are not strategy problems.

They are execution problems.

The Shift: From Consulting to Implementation

Leading private equity firms are starting to rethink their approach.

Instead of asking:

“Who can help us define value creation?”

They’re asking:

“Who can help us deliver it?”

This shift is creating a new category:

Implementation Execution

An execution-focused model that:

- Works inside portfolio companies

- Partners directly with operations teams

- Drives change across the value stream

- Embeds improvements into daily execution

- Delivers measurable financial results

This approach focuses on:

- Speed to EBITDA

- Sustainability of improvements

- De-risking value creation

And it aligns directly with what private equity firms need:

Results within the hold period.

Value Creation Across the PE Lifecycle

The biggest opportunity for value creation isn’t in one phase.

It spans the entire lifecycle:

Pre-Acquisition

- Identify and quantify operational upside

- Validate execution feasibility

- De-risk the investment

Value Creation Phase

- Implement operational improvements

- Drive cost, throughput, and quality gains

- Execute AI and digital initiatives inside operations

Exit Preparation

- Maximize profitability

- Improve operational performance

- Increase valuation multiple

Firms that execute across all three phases outperform.

Because they don’t just plan value creation.

They realize it.

What Real Value Creation Looks Like

When execution is done right, the results are clear.

Across portfolio companies, this looks like:

- 20%+ reductions in cost per unit

- Double-digit increases in throughput

- Millions in annualized savings

- Improved on-time delivery and service levels

For example:

- 31% increase in throughput driving ~$9M in annual benefit

- 22% reduction in labor cost per unit with $5.2M in savings

- 16% increase in productivity with measurable cost reduction

These results don’t come from strategy.

They come from implementation inside operations.

The Bottom Line

Private equity consulting helps define value creation.

But it doesn’t deliver it.

EBITDA is driven by:

- Execution

- Operational change

- Implementation inside portfolio companies

The firms that outperform are not the ones with the best strategies.

They’re the ones that:

- Execute faster

- Implement deeper

- Drive change across the business

Because in private equity:

Value isn’t created in the plan.

It’s created in the execution.

FAQ’s:

Why doesn’t private equity consulting alone drive EBITDA?

Because most consulting engagements stop at planning. They deliver assessments, benchmarking, and a prioritized roadmap with a business case, but they don’t own execution inside the portfolio company. What’s missing is integration into day-to-day operations and sustained operational change. The result is clear plans but limited, delayed, or no EBITDA impact—consistent with research showing 70–90% of strategic initiatives fail to achieve intended value.

Where does value creation typically break down inside portfolio companies?

In the same five places: (1) no ownership for execution at the operational level, (2) limited integration across functions (ops, supply chain, maintenance, quality) that are improved in isolation, (3) lack of frontline adoption into routines, management systems, and standard work, (4) overreliance on leadership alignment without traction on the floor, and (5) time to value that’s too slow for the hold period.

What operational levers actually move EBITDA?

Execution-focused levers: (1) throughput improvement via bottleneck removal, flow optimization, and scheduling; (2) cost reduction that sticks through labor productivity, waste elimination, and process efficiency; (3) asset reliability via predictive maintenance, better maintenance execution, and integrated ops/maintenance; (4) quality and yield through early defect detection, standardized processes, and embedded quality systems; and (5) planning and execution improvements in demand forecasting, production planning, and inventory optimization.

What is “Implementation Execution,” and how is it different from traditional consulting?

It’s an execution-first model that works inside portfolio companies, partners directly with operations teams, drives change across the end-to-end value stream, embeds improvements into daily execution, and delivers measurable financial results. It prioritizes speed to EBITDA, sustainability of improvements, and de-risking value creation—aligning with the need to produce results within the hold period.

How should firms apply this approach across the PE lifecycle, and what results can they expect?

Apply it end-to-end: (1) Pre-acquisition—identify and quantify operational upside, validate execution feasibility, and de-risk the investment; (2) Value creation phase—implement operational improvements, drive cost/throughput/quality gains, and execute AI/digital initiatives inside operations; (3) Exit preparation—maximize profitability, improve operational performance, and lift the valuation multiple. When done right, firms see outcomes like 20%+ reductions in cost per unit, double-digit throughput increases, millions in annualized savings, improved service levels—for example, a 31% throughput increase (~$9M benefit), 22% lower labor cost per unit ($5.2M savings), and a 16% productivity lift.